Unlocked For All Readers: The Sulfur Squeeze: The Iran War’s Hidden Shock Could Send Copper and Agriculture Into a Two-Year Repricing (and reintroducing SAZZ SIGNAL)

The market is still looking at the Iran war through the wrong lens. Most investors see oil, tankers, jet fuel, and the Strait of Hormuz. That is the obvious layer. The more important layer may be sulfur. It is not a headline commodity, which is precisely why it matters. Sulfur sits underneath sulfuric acid, and sulfuric acid sits underneath fertilizer production, copper leaching, nickel processing, and a wide swath of industrial chemistry. What is now unfolding is no longer a niche side effect of war. It is becoming a system-level input shock.

That changes the commodity map. When the market obsesses over crude alone, it misses the second-order chokepoints that actually drive nonlinear repricing. Sulfur is one of those chokepoints. Sulfuric acid is one of the chemical foundations beneath global food production, but it is also essential in important parts of the metals complex. Once sulfur tightens, the shock does not stay in one market. It spreads across fertilizer, metals, and industrial supply chains at the same time.

This is not just a copper story

Copper is where the financial market will likely notice the problem first. Sulfuric acid is essential for the leaching routes used in a large part of global copper production. That matters because copper is usually analyzed through familiar lenses: mine supply, Chinese demand, electrification, inventories, and treatment charges. All of those still matter. But sulfuric acid introduces a different kind of bottleneck. It is not a geology problem. It is a chemistry problem.

And chemistry bottlenecks can be more dangerous because they are often invisible until they become acute. Markets are conditioned to react to mine strikes, weather disruptions, and inventory draws. They are far less prepared for a scenario where the ore is there, the demand is there, but one of the processing inputs becomes scarce enough to constrain output. That is when copper stops behaving like an ordinary cyclical metal and starts behaving like a strategic scarcity asset.

If sulfuric acid remains tight, the copper market does not need a dramatic collapse in mine supply to move sharply higher. It only needs enough marginal output to become uncertain. That is how the forward curve begins to reprice. It is not the total loss of supply that matters first. It is the rising probability that supply becomes less reliable.

The bigger trade may be agriculture

The copper thesis is powerful, but it may not even be the whole trade. The more important expansion of the thesis is agriculture.

Sulfuric acid is indispensable in phosphate fertilizer production. That means any meaningful disruption in sulfur availability will eventually feed into fertilizer costs, crop economics, and food pricing. Once governments realize that sulfur tightness threatens domestic fertilizer supply, the political response changes. This stops being a commodity-market issue and becomes a food-security issue.

That distinction matters. Industrial shortages can be tolerated. Food-related shortages usually trigger intervention. Export restrictions, domestic prioritization, and supply hoarding become more likely. Once major countries begin trying to insulate themselves from the shock, global trade becomes less efficient and global clearing prices move higher. The result is not just volatility. It is stickier, more persistent scarcity.

This is why the sulfur story has the potential to become much bigger than most investors currently appreciate. It does not just affect a mining input. It affects the cost base of the global agricultural system.

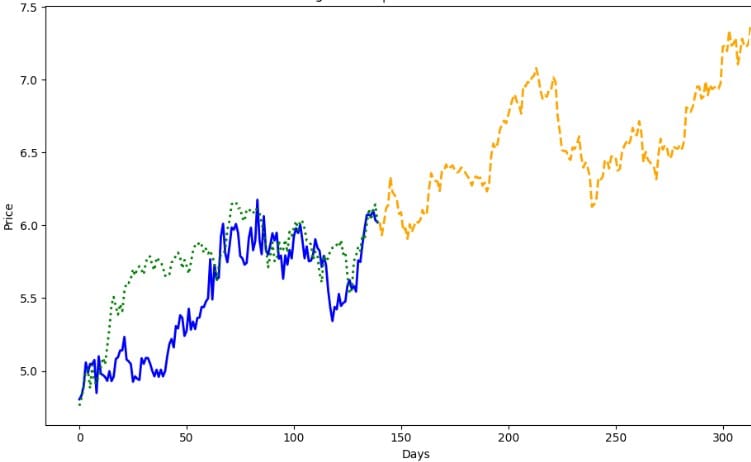

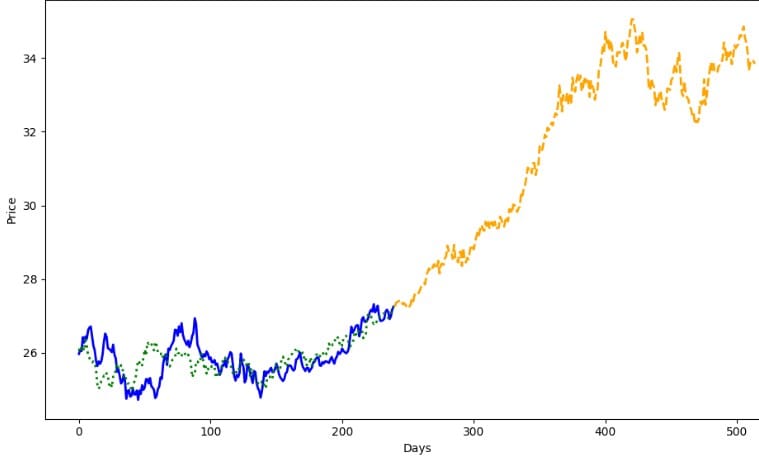

The DBA projection changes the whole framing

This is where the agricultural projection becomes so important. It suggests this is not merely a metals story. It may be the beginning of a broader real-asset repricing cycle.

The projected path for DBA (The Agricultural Fund ETF) points to a sustained move higher over an extended period, not a brief war spike that quickly fades. The pattern suggests an advance that unfolds in stages: periods of upside, pauses that relieve overbought conditions, then renewed pushes higher. In other words, it implies a trend that can persist rather than a one-off panic move.

That has major implications. If the agricultural complex follows that kind of path, it would suggest the market is beginning to absorb not only geopolitical fear, but a deeper shift in input economics. Agriculture would not need a catastrophic crop failure to move materially higher. It would only need fertilizer pressure, supply-chain friction, and policy intervention to keep tightening the system over time.

That is what makes this projection so powerful conceptually. It points toward a slow-burn repricing of agriculture rather than a short-lived headline shock. The likely implication is that food-linked assets could remain structurally supported well beyond the initial phase of the conflict, especially if sulfur-related tightness continues to ripple through fertilizer markets.

Why this could become a two-front commodity bull move

The real edge here is that the same invisible input is now hitting two macro complexes at once. Copper sits inside electrification, grids, defense production, industrial capex, and infrastructure. Agriculture sits inside food inflation, fertilizer demand, and political stability. If sulfur pressure persists, both complexes can reprice together.

That is not an ordinary commodity rally. It is a cross-sector reagent shock.

And that is where the asymmetry lies. Most investors think in terms of headline commodities. They understand oil. They understand natural gas. They understand gold. Far fewer think about the enabling chemicals and byproducts that make the rest of the system function. But hidden inputs are often where the most explosive repricings begin, precisely because they are underfollowed.

If sulfur remains constrained, copper can rise because acid availability constrains output economics. Agriculture can rise because fertilizer costs stay elevated and governments interfere with trade. Nickel and other metals can also feel the squeeze through acid-intensive processing. When one reagent begins transmitting stress across multiple commodity families, the market is no longer dealing with a simple supply disruption. It is dealing with a structural repricing mechanism.

What the market still does not understand

The consensus still seems to believe that this is mostly an oil-and-shipping story. That is too shallow. The real issue is that the war has exposed how dependent modern industry is on low-visibility inputs moving through politically fragile corridors. The Strait of Hormuz is not just an energy artery. It is also part of a much broader industrial plumbing system.

Once that plumbing is disrupted, the consequences spread quietly before they spread visibly. First come price increases in obscure chemical markets. Then come trade restrictions. Then come higher costs for fertilizer, mining, and refining. Then, finally, the large liquid markets begin to react. By the time most participants notice, the repricing is already underway.

That is why the agricultural projection matters so much. It suggests this shock may not end with a ceasefire headline or a temporary shipping workaround. It may be the start of a longer revaluation of agriculture as fertilizer scarcity, export controls, and geopolitical fragmentation begin to work their way through prices over many quarters.

Copper may rally because acid supply constrains leaching. Agriculture may rally because sulfur constraints raise fertilizer costs. In both cases, the common denominator is the same overlooked bottleneck.

The CryptoSazz Pro takeaway

The highest-conviction takeaway is not that oil goes up. The highest-conviction takeaway is that the market may be underestimating a deeper reagent shock moving through the global commodity system. Copper remains a high-quality expression of that theme because sulfuric acid shortages can impair supply and tighten the marginal production curve. But the agricultural projection argues that food and farm-input exposure may be an equally important, and potentially longer-duration, expression of the same idea.

If that projected path is even directionally correct, the bigger story is no longer just about metals. It is about the repricing of the physical economy itself. It is about the cost of extracting metal, producing fertilizer, and growing food all being pressured by a single hidden chokepoint.

That is the kind of shift markets rarely price early. They price it late, when inventories are already tighter, governments are already restricting exports, and the clean entry has already passed. Right now, the sulfur story still sits in the blind spot. And that is exactly why it matters.

And one more thing for readers who want actionable market intelligence rather than delayed mainstream narratives: due to high demand, SAZZ Signal is back. This is our entry-level tier for investors who want sharper positioning, faster interpretation, and high-value insights without stepping up to the full Pro product. SAZZ Signal is now available at $19/month or $190/year.

✍️ By The CryptoSazz Markets Desk

The content provided on CryptoSazz is for informational and educational purposes only and does not constitute financial, investment, trading, or other advice. Nothing on this site is a recommendation or solicitation to buy or sell any financial asset or to adopt any investment strategy.

CryptoSazz may discuss market trends, macroeconomic developments, and quantitative trading models; however, these are intended solely to share insights and analysis and are not tailored to your specific financial situation or investment objectives.

While we strive to ensure the accuracy and timeliness of the information presented, CryptoSazz makes no warranties or representations regarding its completeness or reliability. All opinions expressed are subject to change without notice.

Cryptocurrencies, DeFi protocols, and digital assets involve significant risk, including the potential loss of principal. You should conduct your own research and consult a qualified financial advisor before making any investment decisions.

Past performance is not indicative of future results.